What Are GST and PST in Canada?

GST stands for Goods and Services Tax, while PST refers to Provincial Sales Tax. These are two primary taxes applied to the sale of goods and services in Canada. The GST is a federal tax, meaning it is collected by the government of Canada and is applicable across all provinces. Typically, the GST rate is 5%, and it applies to most goods and services throughout the country.

On the other hand, PST is a tax that is levied by individual provinces. The rate and application of PST can vary significantly from one province to another. For instance, in British Columbia, the PST is 7%, while in Saskatchewan, it is set at 6%. Some provinces, like Alberta, do not impose a PST. When invoicing in Canada, businesses need to clearly indicate the GST and PST, if applicable, as separate line items to ensure transparency and compliance with tax regulations.

A practical example can be seen with a business operating in British Columbia. If they sell an item worth $100, they would charge 5% GST, amounting to $5, and 7% PST, which amounts to $7. This brings the total invoice amount to $112. It's crucial for businesses to understand these tax requirements to avoid penalties and ensure proper tax collection and remittance. According to houseblend.io, understanding the "place of supply" rules is critical for correct tax application.

Differences Between GST, PST, and HST

While GST and PST are often discussed in tandem, it's important to differentiate them from HST, the Harmonized Sales Tax. HST is a combination of the GST and PST into a single tax applied in provinces that have chosen to harmonize these taxes. This tax simplifies the tax process by combining federal and provincial taxes into one, with a unified rate, making it easier for businesses to manage.

HST is utilized in provinces like Ontario, New Brunswick, and Newfoundland and Labrador. For example, in Ontario, the HST is set at 13%, which covers both the 5% federal GST and an 8% provincial component. This eliminates the need for businesses to separately account for GST and PST, streamlining the invoicing process. However, in non-HST provinces, businesses must calculate and list both GST and PST separately on invoices, which can add complexity.

Choosing between GST/PST and HST depends largely on the province in which a business operates. Each has its own implications for invoicing and compliance. For businesses operating across multiple provinces, understanding these nuances is crucial. According to canada.ca, understanding these distinctions is essential for proper tax compliance and avoiding potential legal issues.

How to Register for GST/PST in Canada

Registering for GST and PST in Canada involves a few clear steps, and it's a crucial process for businesses exceeding specific revenue thresholds. To start, any business with worldwide taxable revenues over CAD 30,000 in a single calendar quarter or over four consecutive quarters must register for GST. The process can be initiated through the Canada Revenue Agency (CRA) website, where businesses can apply for a GST/HST account number.

For PST, the requirements and procedures can differ depending on the province. For example, in British Columbia, businesses must apply for a PST number through the province's tax authority. Documentation such as proof of business registration and identification is typically required. It's important to gather all necessary documents before starting the registration process to avoid delays.

A practical tip for successful registration is to ensure all business information is accurate and up-to-date. Mistakes in registration details can lead to processing delays and potential fines. Businesses should also consider the potential benefits of registering voluntarily if they fall below the mandatory revenue threshold. This can allow them to claim input tax credits on business expenses, which can be a significant financial advantage. For further guidance on registration requirements, visiting airwallex.com can provide valuable insights.

Tax Exemptions and Special Cases

In Canada, there are several instances where businesses might be exempt from charging GST or PST, or where special cases apply. Understanding these exemptions can save time and resources, and help in maintaining compliance. One common exemption is the small supplier threshold. Businesses that have global revenues under CAD 30,000 over four consecutive calendar quarters are not required to register for GST, though they may choose to do so voluntarily to claim input tax credits.

Certain goods and services are also zero-rated or exempt from GST/PST. Zero-rated goods, such as basic groceries and prescription drugs, are taxable at 0%, meaning businesses can claim input tax credits on their purchases. Exempt goods and services include residential rents and certain health care services, where GST/PST is not charged, and input tax credits cannot be claimed.

Additionally, some provinces have specific exemptions. For example, in Saskatchewan, PST exemptions exist for items like agricultural equipment and production machinery. These exemptions can vary widely, so it's essential for businesses to stay informed about the applicable rules in their specific province. According to tmasmallbusinessaccounting.com, understanding these specific exemptions is crucial for accurate invoicing and tax compliance.

Impact of GST/PST on International Sales

GST/PST can significantly impact international sales for Canadian and European businesses, primarily through the rules around charging tax to foreign clients. In Canada, GST/HST is generally not charged on exports or sales to foreign customers if the goods or services are purchased while the customer is outside of Canada. This is advantageous for Canadian businesses aiming to expand their market internationally without the added complexity of charging local taxes. However, businesses must maintain detailed records to substantiate these zero-rated transactions.

In Europe, the situation is somewhat similar but can vary across member states due to different VAT thresholds and rules. Under the EU VAT Directive, VAT is typically not charged on B2B intra-EU supplies when the customer provides a valid VAT identification number. Instead, the reverse charge mechanism applies, shifting the tax liability to the buyer. This rule helps businesses avoid double taxation and maintain competitiveness in international markets. However, it requires businesses to verify VAT numbers and ensure compliance with local VAT laws.

For example, in the EU, electronic invoicing is becoming increasingly mandatory, with countries like Italy already implementing B2B e-invoicing requirements. This shift towards digital invoicing aims to simplify cross-border trade and enhance VAT revenue collection. According to esker.com, e-invoicing is set to become mandatory across the EU from 2028, aligning with the broader "VAT in the Digital Age" strategy. This means Canadian businesses dealing with European clients need to stay informed and prepared for these regulatory changes.

GST/PST Compliance Requirements

Compliance with GST/PST regulations involves precise record-keeping and reporting obligations for businesses. In Canada, businesses must register for GST/HST if their worldwide taxable revenues exceed CAD 30,000 in a single quarter or over four consecutive quarters. Once registered, companies must charge GST/HST on taxable supplies and can claim input tax credits (ITCs) on expenses. This process requires meticulous documentation to support tax filings and avoid penalties.

For European businesses, adhering to the EU VAT Directive is crucial. This regulation mandates that all invoices include specific details such as the supplier's VAT number, invoice number, issue date, and supply date. VAT must be shown separately unless the transaction is exempt or subject to the reverse charge. The complexity of these requirements often varies by country, adding layers of compliance for businesses operating across multiple jurisdictions.

One practical tip for maintaining compliance is to use digital tools to automate tax calculations and invoicing. These tools can ensure that correct tax rates are applied and that invoices meet all regulatory requirements. Moreover, electronic invoicing is becoming a standard in Europe, with mandatory adoption set for 2028 as part of the "VAT in the Digital Age" initiative. According to thomsonreuters.com, more than 80 countries are moving towards mandatory e-invoicing, highlighting the global trend towards digital tax compliance.

Common Mistakes to Avoid in GST/PST Invoicing

Handling GST/PST invoicing can be fraught with pitfalls if not managed carefully. One common mistake businesses make is applying incorrect tax rates, which can lead to overcharging or undercharging customers. For example, failing to adhere to the "place of supply" rule in Canada can result in applying the wrong provincial tax rate. Each province has different tax requirements, and businesses must apply the rate relevant to the customer's location, not the seller's.

Another frequent error is omitting essential tax information on invoices. The Canada Revenue Agency (CRA) requires that invoices show the business name, address, GST/HST registration number, invoice date, and a breakdown of tax amounts. Failure to include these can result in compliance issues and unhappy customers unable to claim input tax credits. Similarly, in Europe, missing VAT numbers or incorrect invoice formatting can lead to automatic rejections and compliance penalties.

To avoid these issues, businesses should consider using automated invoicing software that applies correct tax rates and formats invoices according to regulatory standards. This can significantly reduce the likelihood of errors. According to airwallex.com, automated tools not only help in ensuring compliance but also streamline the invoicing process, saving businesses time and reducing the risk of costly mistakes.

Getting Started with GST/PST in Harvest

Using Harvest to manage GST/PST in your invoicing process can simplify compliance and improve accuracy. With its robust features, Harvest allows you to configure tax settings that automatically apply the correct tax rates based on the location of your clients. This automation is crucial for businesses dealing with multiple tax jurisdictions, like those in Canada, where different provinces have different rates.

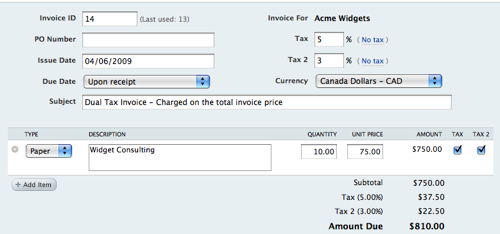

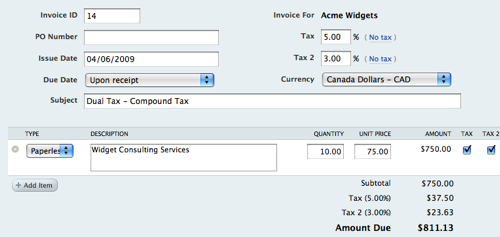

To get started, navigate to the invoicing section within Harvest and set up your tax settings. Here, you can choose between Simple Tax and Compound Tax options, depending on your business location. For instance, businesses operating in Quebec or PEI should opt for Compound Tax, which takes into account both federal and provincial taxes. This ensures that your invoicing aligns with local tax laws, reducing the risk of errors.

Harvest's platform also integrates with popular accounting tools like QuickBooks and Xero, allowing for seamless data transfer and further reducing manual entry errors. Across the 70,000+ teams using Harvest, those who track time and expenses accurately report 25% fewer billing disputes. By adopting these practices, your team can focus more on core business activities rather than administrative tasks. For more information on Harvest's invoicing capabilities, visit Harvest's invoicing page. By leveraging Harvest's tools, you can enhance your invoicing process while ensuring compliance with GST/PST regulations.

Frequently Asked Questions

What is the difference between GST and HST?

GST (Goods and Services Tax) is a federal tax applied to most goods and services in Canada at a rate of 5%. HST (Harmonized Sales Tax) combines the GST with provincial sales taxes in certain provinces, resulting in a higher total tax rate. HST is applicable in provinces like Ontario, New Brunswick, and Nova Scotia, where the combined rate can be up to 15%.

How do I register for GST in Canada?

To register for GST in Canada, you can apply online through the Canada Revenue Agency (CRA) website, by mail, or by phone. You need to provide your business number and information about your business activities. Registration is mandatory if your taxable sales exceed $30,000 in a year, and it allows you to collect GST from customers and claim input tax credits.

What are the tax rates for different provinces in Canada?

Tax rates for GST and HST vary by province. The federal GST rate is 5%, while provinces with HST have rates ranging from 13% to 15%. For example, British Columbia has a PST of 7% in addition to the GST, making the total 12%. It's essential to check the specific rates for each province to ensure compliance.

Are there exemptions for small businesses regarding GST/PST?

Yes, small businesses in Canada can benefit from exemptions regarding GST/PST. If your taxable revenues are under $30,000 in the last four consecutive quarters, you may not need to register for GST. Additionally, certain goods and services may be exempt from GST/PST altogether, such as basic groceries and certain health care services.